After years of working with clients through inheritances, business sales, liquidity events, and other significant financial transitions, we’ve observed that these moments often unfold in remarkably similar ways.

An inheritance arrives unexpectedly. A business is sold. A concentrated stock position suddenly becomes liquid. In the weeks that follow, important financial decisions begin competing with emotion, urgency, outside opinions, and lifestyle changes.

None of that is unusual.

What matters most is not simply the size of the windfall, but how decisions are approached in the period immediately after it arrives.

For many families, those early decisions can influence whether a windfall becomes a lasting foundation for future generations—or simply a temporary change in lifestyle.

The First 90 Days Often Matter Most

One of the most important considerations after receiving a financial windfall is resisting the pressure to act too quickly.

In our experience, the first few months following a significant financial event are often when emotions can outweigh long-term thinking. Behavioral finance researchers sometimes refer to this tendency as the “house money effect,” where unexpected wealth is treated differently than money accumulated gradually over time.

That can lead to decisions that may not fully reflect long-term priorities.

Common patterns we often see include:

Major lifestyle purchases made before a broader financial strategy is established

Investment decisions influenced by outside opinions or recent market enthusiasm

Financial support for family members offered before long-term implications are evaluated

Delayed decision-making caused by uncertainty, grief, or emotional fatigue

Sometimes the challenge is overspending. Other times it is complete paralysis.

Both can create unintended consequences.

Five Patterns We Commonly Observe

Every client situation is different. Still, certain themes emerge repeatedly during periods of sudden wealth or financial transition.

1. The Lifestyle Expansion

Lifestyle changes are often one of the first instincts after receiving significant wealth.

A new home, travel, renovations, vehicles, or other upgrades may all be reasonable decisions on their own. The challenge arises when permanent lifestyle commitments are made before understanding what level of spending can realistically be sustained long term.

In some cases, a windfall that could have strengthened long-term financial independence instead becomes tied to recurring expenses that require continued income to support.

The question is rarely whether someone can afford something today.

The more important question is whether those decisions continue supporting broader financial goals years from now.

2. The Pressure to Help Everyone

Generosity is often one of the most meaningful aspects of financial success or inheritance.

At the same time, sudden wealth can create emotional pressure from family members, friends, or others seeking financial assistance.

Thoughtful gifting strategies can absolutely play an important role in estate and legacy planning. But there is an important difference between:

strategic giving aligned with long-term goals and emotionally driven decisions made before a plan is in place

When appropriate, these conversations are often best approached deliberately and with coordination between financial, tax, and legal professionals.

3. The “I’ll Manage It Myself” Phase

Some individuals receiving a windfall consider managing the assets independently, particularly if they have not previously worked with an advisor.

That instinct is understandable. But substantial liquidity events often introduce complexities that extend beyond investment management alone, including:

tax considerations

estate implications

income planning

risk management

charitable strategies

business succession planning

and multi-generational coordination

In many situations, the value of professional guidance is less about market predictions and more about helping ensure decisions remain coordinated and aligned over time.

4. The Emotional Weight of Inheritance

Not every windfall feels exciting.

For many inheritors, wealth arrives alongside grief, family complexity, or emotional responsibility. Decisions that may appear straightforward on paper can become difficult because of the emotional meaning attached to the assets themselves.

In some cases, families delay decisions for years—not because they lack intelligence or resources, but because the emotional burden feels significant.

A thoughtful planning process can help create structure during periods that otherwise feel overwhelming.

5. The Families Who Tend to Navigate It Best

The families who appear to navigate windfalls most effectively often share several common traits.

They:

pause before making major commitments

communicate openly about priorities and expectations

assemble experienced professionals early

think long term rather than react emotionally

remain intentional about lifestyle decisions

and approach wealth as a tool tied to broader values and objectives

In many cases, the strongest outcomes come not from making rapid decisions, but from making coordinated ones.

Why This Conversation Is Becoming More Important

The ongoing generational wealth transfer is expected to reshape financial planning conversations for decades.

For many families, these transitions may occur during already complicated stages of life:

caring for aging parents

supporting adult children

preparing for retirement

managing businesses

or navigating estate responsibilities

As a result, these situations often require more than isolated financial advice. They require coordination, perspective, and thoughtful decision-making across multiple areas of financial life.

A Framework for Navigating a Windfall

While every situation is unique, we often encourage clients to think through several foundational steps:

1. Pause Before Major Decisions

Avoid feeling pressured to act immediately.

2. Assemble the Right Team

Coordinate with financial, tax, and legal professionals early.

3. Clarify Long-Term Priorities

Define what the wealth is ultimately intended to support.

4. Evaluate the Full Financial Picture

Review taxes, liabilities, estate considerations, investment structure, and liquidity needs together—not separately.

5. Create Space for Intentional Decisions

Thoughtful planning often produces better outcomes than reactive decision-making.

The Bottom Line

A financial windfall can create tremendous opportunity. It can also introduce complexity, emotional pressure, and important long-term decisions.

In our experience, the families who navigate these transitions most effectively are often those who approach them deliberately—with perspective, coordination, and a clear understanding of what the wealth is ultimately meant to support.

Frequently Asked Questions About Financial Windfalls

How long should I wait before making major financial decisions after receiving a windfall?

In many situations, it can be beneficial to pause before making significant financial commitments or investment decisions. Taking time to assemble the appropriate advisory team, evaluate tax considerations, and clarify long-term priorities often creates more flexibility and perspective than reacting immediately under pressure.

What are the most common mistakes families make after receiving a large inheritance or liquidity event?

Some of the most common challenges include:

making significant lifestyle changes too quickly

offering financial support to others before a long-term strategy is established

overlooking tax implications in the first year

making investment decisions based on emotion or outside influence

delaying decisions entirely due to uncertainty, grief, or emotional fatigue

In our experience, thoughtful coordination early on can help reduce unintended long-term consequences.

Should I work with multiple professionals after receiving a windfall?

Major financial transitions often involve investment, tax, estate, legal, and planning considerations simultaneously. Coordinating with financial advisors, CPAs, and estate planning attorneys can help ensure decisions remain aligned across all areas of your financial life.

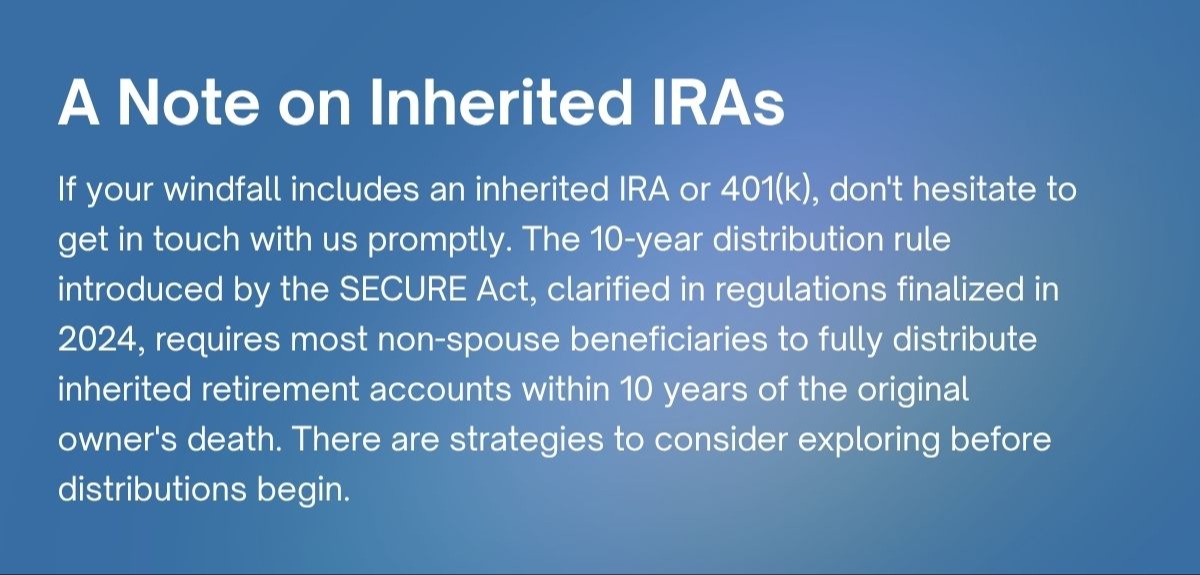

What taxes apply to inheritances, business sales, or other financial windfalls?

Tax treatment varies depending on the type of windfall, how assets are structured, and individual circumstances. Inheritances, business sales, stock compensation, real estate transactions, and retirement accounts can all carry different tax considerations. Reviewing these issues early with qualified tax and legal professionals is often an important part of the planning process.

What should I do first after receiving an inheritance or liquidity event?

One of the first priorities is often creating space to evaluate the situation carefully before making major financial decisions. This may include:

securing liquidity appropriately

understanding tax implications

reviewing estate considerations

identifying immediate cash flow needs

and clarifying long-term objectives before implementing a broader strategy

How can families prepare for a future wealth transfer before it happens?

Many families benefit from beginning conversations early—before a major transfer occurs. Discussions around estate structure, beneficiary planning, family communication, philanthropic goals, and long-term intentions can help reduce confusion and improve coordination when wealth eventually transfers.

Can a financial windfall affect long-term retirement or estate planning?

Yes. Significant liquidity events can reshape retirement planning, investment strategy, estate considerations, charitable planning, and multi-generational wealth transfer decisions. Reviewing these areas together within a coordinated framework can help ensure decisions support broader long-term objectives.

We’re Here for You Before, During, or After a Windfall

At OakStreet Capital Management, we work with individuals, families, and business owners navigating complex financial decisions and long-term planning considerations.

If you are preparing for—or currently experiencing—a significant financial transition, we welcome the opportunity to start a conversation

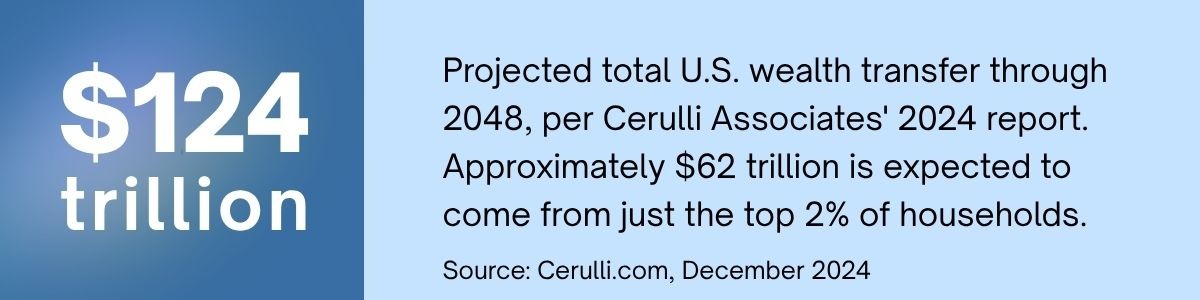

Sources:

Cerulli.com, December 2024

https://www.cerulli.com/press-releases/cerulli-anticipates-124-trillion-in-wealth-will-transfer-through-2048

PMC PubMed Central, April 2026

https://pmc.ncbi.nlm.nih.gov/articles/PMC12272607/

CitizensBank.com, April 2026

https://www.citizensbank.com/learning/great-wealth-transfer-survey.aspx

Glenmede.com, December 22, 2025

https://www.glenmede.com/insights-private-wealth/the-great-generational-wealth-transfer/

Empower.com, April 13, 2026

https://www.empower.com/the-currency/money/spending-a-windfall-research

CAPTrustAtWork.com, April 2026

https://www.captrustatwork.com/suddenly-in-the-money/

Fortune.com, July 23, 2025

https://fortune.com/2025/07/23/great-wealth-transfer-124-trillion-bigger-than-ever-millennials-gen-x/