The Retirement Conversation Couples Keep Avoiding

As financial professionals, we spend much of our time helping clients prepare for retirement. By the time many people are within a few years of retirement, the visible pieces are often already in place—investment accounts have grown, savings goals are largely met, and the numbers on paper appear reasonable.

But there is another side of retirement planning that is often less discussed.

It is not simply:

how much you have saved

or

when you plan to stop working

It is whether the two of you have truly talked through what retirement will actually look like.

Where will you live?

Will you retire at the same time?

How will you spend your days?

What role will family, travel, health, purpose, or work continue to play?

And are both partners envisioning the same future?

In our experience, many couples have not fully explored those questions together.

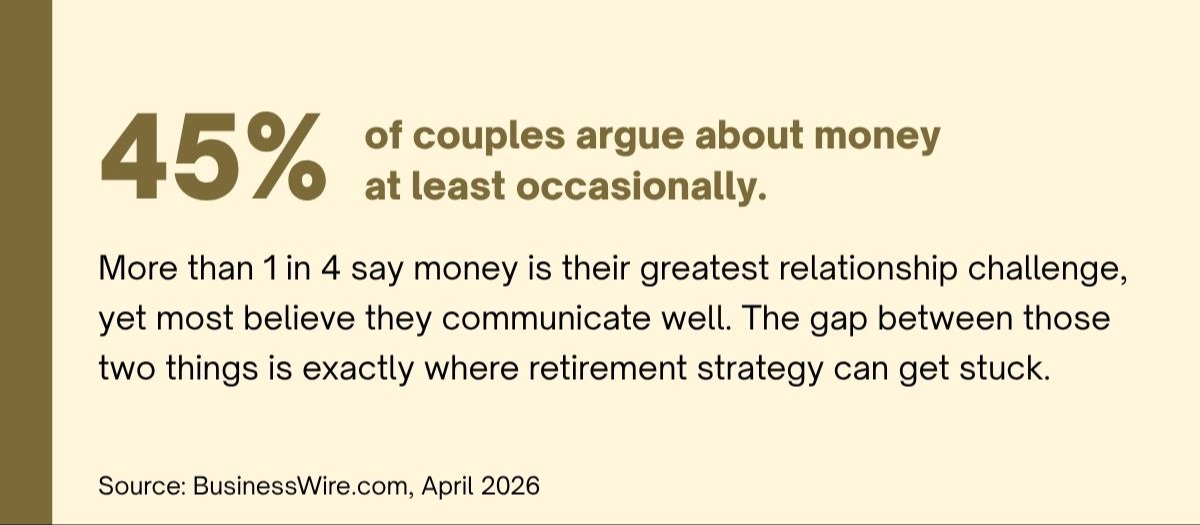

Research suggests these conversations matter more than many people realize. Financial disagreements and differing expectations can create stress well before retirement begins—and often become more visible during major life transitions.

These are rarely “small” gaps.

Over time, they can influence:

retirement timing

spending decisions

healthcare planning

estate considerations

and overall confidence about the future

The Timing Conversation Many Couples Avoid

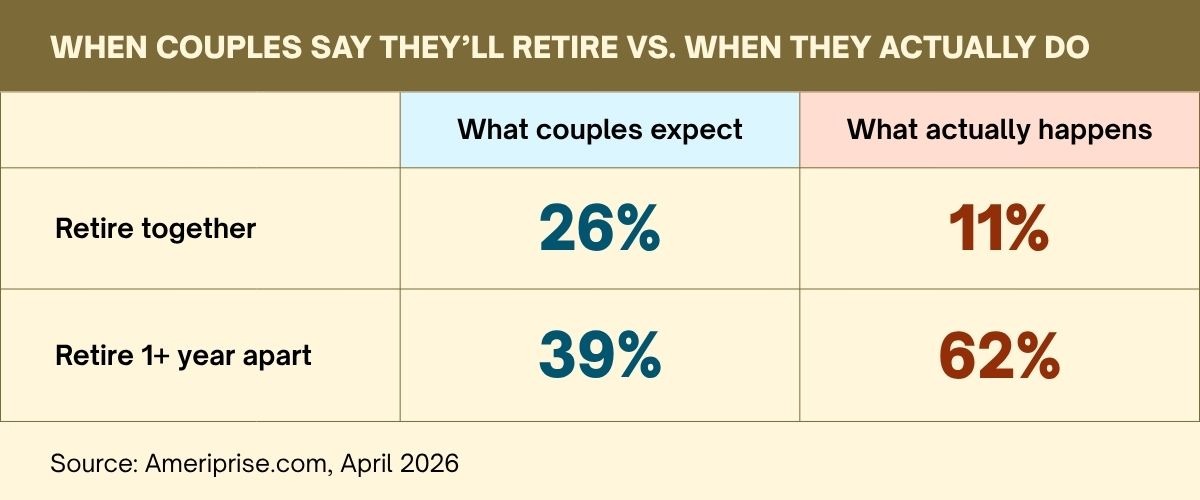

One of the most common assumptions couples make is that they will retire at roughly the same time.

In practice, that often does not happen.

Sometimes one partner enjoys work longer than expected. Sometimes healthcare coverage, compensation, or financial considerations create incentives for staggered retirement timing. In other situations, one spouse may simply feel emotionally more prepared for retirement than the other.

The result is that retirement may unfold in stages rather than as a single shared transition.

That shift can affect household dynamics in ways many couples do not anticipate:

daily routines change

financial responsibilities may shift

social structure evolves

and each partner’s expectations around independence and time together may differ

These are not necessarily problems. In many cases, staggered retirement can actually create flexibility and financial advantages.

But the transition tends to go more smoothly when those conversations happen intentionally before retirement begins rather than after assumptions collide with reality.

Important Questions Worth Discussing Before Retirement

Where Will We Live—and Have We Both Fully Agreed?

This conversation often carries some of the largest financial and lifestyle implications in retirement planning.

One partner may envision relocating closer to children or grandchildren. The other may prefer remaining near long-established social networks, healthcare providers, or community ties.

Housing decisions can affect:

cost of living

taxes

healthcare access

estate planning

lifestyle flexibility

and long-term financial sustainability

The important point is not simply making a decision—it is making sure both partners are working from the same assumptions.

How Will We Create Structure and Purpose in Retirement?

Retirement changes more than income. It often changes identity, routine, and daily structure.

For some individuals, that transition feels freeing. For others, it can feel unexpectedly disorienting.

The retirees who appear to navigate this transition most smoothly are often those who have already thought intentionally about:

purpose

relationships

physical activity

intellectual engagement

travel

volunteer work

consulting

family involvement

or other meaningful pursuits

Retirement is not simply about leaving work. It is about replacing the structure work once provided.

This can also affect the relationship itself. Couples who suddenly spend significantly more time together sometimes discover they need more intentional balance between togetherness and personal independence than they previously expected.

How Will We Prepare for Healthcare Costs and Decisions?

Healthcare remains one of the most significant and often underestimated retirement expenses.

Beyond the cost itself, many couples are surprised by the complexity of:

Medicare decisions

supplemental coverage

long-term care considerations

income-related premium adjustments

and healthcare coordination between spouses with different retirement timelines

These decisions are often interconnected with broader retirement income and tax planning considerations.

Preparing early can create more flexibility than making rushed decisions close to enrollment deadlines or during periods of health stress.

What Happens if One of Us Needs Extended Care?

Long-term care conversations are among the most commonly delayed discussions in retirement planning.

Not because couples do not care about the issue—but because discussing aging, illness, or dependency can feel emotionally difficult.

Yet these conversations often become more manageable when addressed proactively rather than during a crisis.

The important question is usually not:

“Which facility would we prefer?”

It is:

“How would this affect our broader financial strategy, and have we prepared thoughtfully for that possibility?”

Extended care planning can influence:

retirement income strategy

investment planning

estate structure

gifting intentions

and financial flexibility later in life

How Will We Coordinate Social Security Decisions?

Social Security decisions are more nuanced than simply selecting the earliest or latest possible claiming age.

For couples, claiming strategies can affect:

household income

survivor benefits

tax planning

portfolio withdrawals

and long-term retirement cash flow

In many situations, the optimal strategy depends on the coordination between both spouses’ earnings histories, health considerations, income needs, and broader retirement objectives.

The right decision is often less about maximizing a single benefit calculation and more about integrating Social Security into an overall retirement framework.

Do We Have a Coordinated Financial Strategy?

One of the most overlooked aspects of retirement planning is ensuring that all pieces of the financial picture work together cohesively.

Retirement decisions often intersect with:

investment management

tax planning

estate strategy

healthcare considerations

charitable intentions

business succession planning

and multi-generational wealth transfer goals

When these decisions are approached separately, important gaps can emerge over time.

A coordinated strategy helps ensure financial decisions remain aligned with broader long-term priorities.

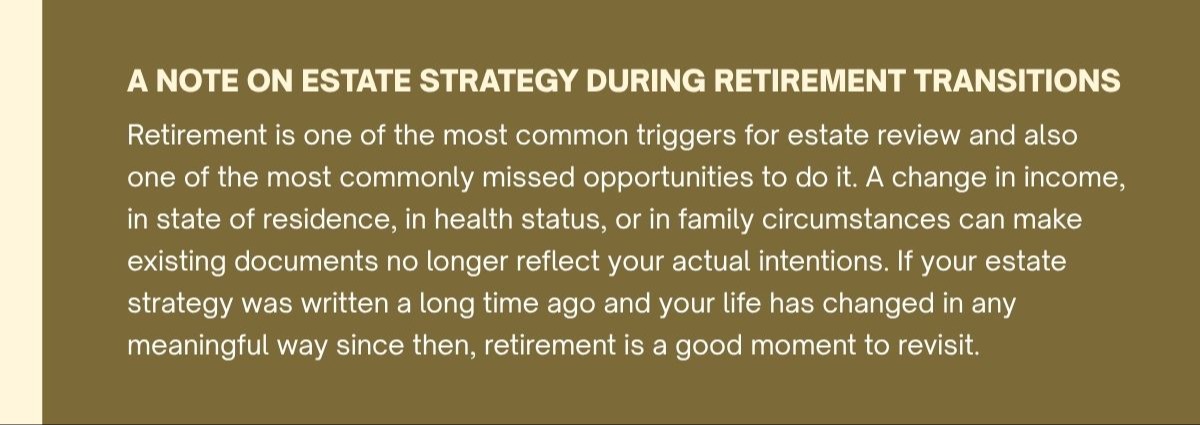

Retirement Is Often a Good Time to Revisit Estate Planning

Retirement is also one of the most common periods for reviewing estate documents and beneficiary structures.

Changes in:

residence

family dynamics

health

asset structure

or long-term objectives

can all create reasons to revisit existing planning documents.

For many families, retirement becomes a natural transition point to review:

wills

trusts

powers of attorney

healthcare directives

beneficiary designations

and broader legacy intentions

What Productive Retirement Conversations Often Look Like

One of the benefits of discussing retirement planning within a structured advisory setting is that it creates space for conversations couples may otherwise avoid.

In our experience, most couples are not actually as far apart as they initially believe.

Often:

both partners value financial security

both care deeply about family

both want flexibility and independence

and both are trying to protect the future

The disconnect usually comes from assumptions that have never been fully discussed out loud.

The most productive retirement conversations tend to happen when couples approach the process collaboratively rather than defensively—remaining open to learning what matters most to one another before making major financial decisions.

Frequently Asked Questions About Retirement Planning for Couples

What should couples discuss before retirement?

Some of the most important retirement conversations include:

retirement timing

where you plan to live

healthcare planning

Social Security coordination

estate strategy

lifestyle expectations

and how each partner hopes to spend time in retirement

These discussions often become easier when addressed gradually and intentionally before retirement begins.

Is it normal for couples to disagree about retirement plans?

Yes. Couples frequently have different expectations around spending, travel, family support, work, or lifestyle priorities in retirement.

Disagreement itself is not unusual. The more important issue is whether those differences are identified and discussed early enough to allow thoughtful planning and compromise.

How often should retirement and estate plans be reviewed?

Retirement and estate planning strategies often benefit from periodic review, particularly after major life events such as:

retirement

relocation

health changes

inheritance

business sales

family structure changes

or significant market and tax law developments

Many families review these areas annually or whenever meaningful life transitions occur.

What healthcare costs should couples prepare for in retirement?

Healthcare costs can include:

Medicare premiums

supplemental insurance

prescription expenses

long-term care considerations

and out-of-pocket medical costs

Because healthcare decisions often intersect with tax planning, retirement income strategy, and long-term financial planning, many couples benefit from evaluating these areas together rather than independently.

What is the biggest mistake couples make when planning for retirement?

One of the most common challenges is assuming both partners share the same expectations without fully discussing them.

Retirement planning is not only financial—it is also deeply personal. Conversations around lifestyle, purpose, family priorities, healthcare, and long-term goals are often just as important as investment and income planning decisions.

The Time to Start These Conversations Is Before Retirement Arrives

Retirement is one of the most significant transitions many couples will experience. The financial side matters deeply—but so do the conversations surrounding lifestyle, priorities, family, health, and long-term expectations.

In our experience, couples who approach retirement most confidently are often those who take time to communicate intentionally, plan thoughtfully, and coordinate decisions within a broader long-term strategy.

At OakStreet Capital Management, we work with individuals, families, and business owners navigating complex retirement, investment, and planning decisions.

If you are approaching retirement and would like to begin a more thoughtful conversation about the years ahead, we welcome the opportunity to connect.

Sources:

BusinessWire.com, April 2026

https://www.businesswire.com/news/home/20240201922762/en/Love-Money-Most-Couples-Give-Themselves-High-Marks-in-Communication-Yet-Fidelity-Study-Reveals-Hidden-Frustrations-in-Couples-Financial-Future

Ameriprise.com, April 2026

https://www.ameriprise.com/binaries/content/assets/ampcom/amp_research-report.pdf

NewsRoom.Fidelity.com, July 30, 2025

https://newsroom.fidelity.com/pressreleases/fidelity-investments--releases-2025-retiree-health-care-cost-estimate--a-timely-reminder-for-all-gen/s/3c62e988-12e2-4dc8-afb4-f44b06c6d52e

NerdWallet.com, January 15, 2026

https://www.nerdwallet.com/insurance/medicare/learn/what-is-the-medicare-irmaa?msockid=37a2e58496ac672b39a4f4af9742667d

AARP.org, March 12, 2026

https://www.aarp.org/caregiving/financial-legal/long-term-care-affordability-report/

CFSWV.com, January 2, 2024

https://cfswv.com/cfsblog/long-term-care-statistics-to-know-for-2024

Financial-Planning.com, April 19, 2024

https://www.financial-planning.com/news/quarter-of-couples-disagree-over-retirement-spending-priorities